Home Mortgage Guidance That Can Save You A Bundle

Created by-Barlow JohnstonOne of the great joys in life is buying a home. Most people wanting to purchase their own home will have to get a loan. This process can seem quite confusing and lengthy. Keep on reading to learn how to get the right home mortgage.

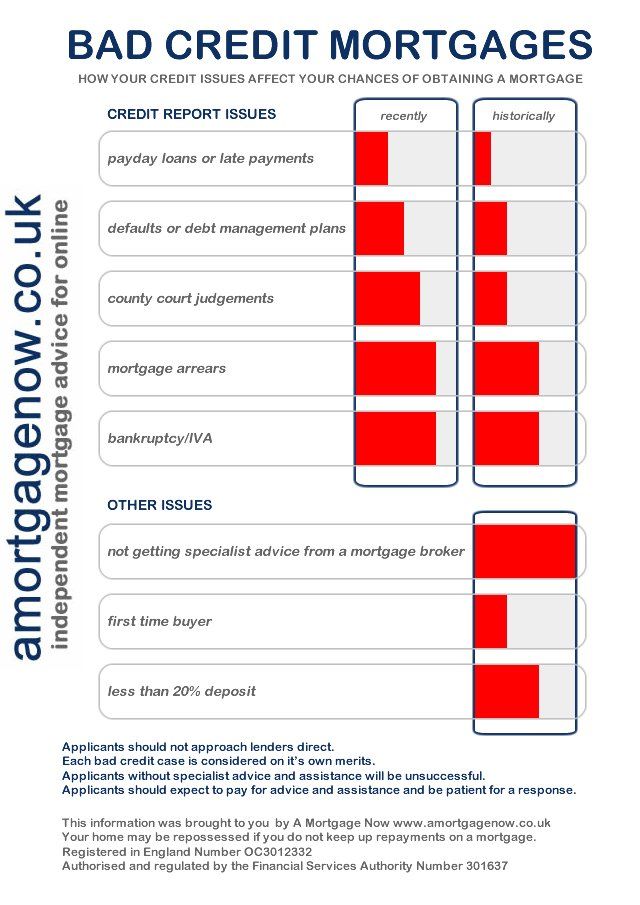

Before trying to get a mortgage approval, find out your credit score. Mortgage lenders can deny a loan when the borrower has a low credit score caused by late payments and other negative credit history. If your credit score is too low to qualify for a mortgage loan, clean up your credit, fix any inaccuracies and make all your payments on time.

Do not waste time in your home mortgage process. After you've submitted a mortgage application to the lender, this is when your clock start ticking. You have to send any necessary documents for the application process quickly. Any delays could destroy a purchase and cost you your deposit. Get an expected closing date, and then keep in touch with the lender periodically until your loan closes. Some lenders close quicker than others.

Before getting a mortgage, study your credit history. Good credit is what can help you get a mortgage. Obtain copies of your credit history and scores from the three major credit-reporting bureaus. Study your reports carefully to ensure that no issues or errors must be resolved before you apply. Many lenders need a minimum score of 680, which complies with Freddie Mac and Fannie Mae's guidelines. Most lenders want to avoid scores that are lower than 620.

Find out how much your mortgage broker will be making off of the transaction. Many times mortgage broker commissions are negotiable just like real estate agent commissions are negotiable. Get this information and writing and take the time to look over the fee schedule to ensure the items listed are correct.

Don't make any sudden moves with your credit during your mortgage process. If your mortgage is approved, your credit needs to stay put until closing. After a lender pulls up your credit and says you're approved, that doesn't mean it's a done deal. Many lenders will pull your credit again just before the loan closes. Avoid doing anything that could impact your credit. Don't close accounts or apply for new credit lines. Be sure to pay your bills on time and don't finance new cars.

Try shopping around for a home mortgage. When you do shop around, you need to do more than just compare interest rates. While they're important, you need to consider closing costs, points and the different types of loans. Try getting estimates from a few banks and mortgage brokers before deciding the best combination for your situation.

Use local lenders. If you are using a mortgage broker, it is common to get quotes from lenders who are out of state. Estimates given by brokers who are not local may not be aware of costs that local lenders know about because they are familiar with local laws. This can lead to incorrect estimates.

Speak with many lenders before selecting the one you want to borrow from. Know what these lenders are all about, and check with family and friends to get a good picture on what they will charge you. After you have all the information, you can make a smart choice.

Make sure you pay down any debts and avoid new ones while in the process of getting approved for a mortgage loan. Before a lender approves you for a mortgage, they evaluate your debt to income ratio. If your debt ratio is too high, the lender can offer you a lower mortgage or deny you a loan.

If your mortgage has you struggling, seek assistance. Think about getting financial counseling if you are having problems making payments. Counseling agencies are available to you wherever you may live and many are sponsored by HUD. With the help of HUD-approved counselors, you can get free counseling for foreclosure-prevention. Look online or call HUD to find the nearest office.

Do not even bother with looking at houses before you have applied for a home mortgage. When you have pre-approval, you know how much money you have to work with. Additionally, pre-approval means you do not have to rush. You can take your time looking at homes knowing that you have money in your pocket.

Do not embark on the process of buying a home if you have just started a new job within the last year. The best home mortgage rates go to those that have been with a company for a number of years. Having a job for a short time is seen as a risk, and you will be the one to pay for it with a higher interest rate.

Avoid interest only type loans. With an interest only loan, the borrower only pays for the interest on the loan and the principal never decreases. This type of loan may seem like a wise choice; however, at the end of the loan a balloon payment is needed. This payment is the entire principal of the loan.

Many lenders now require a home to be inspected before the loan is approved. Although https://www.bai.org/banking-strategies/article-detail/small-business-lending-fraud-is-a-big-deal/ costs a small amount of money, it can save you thousands in unknown expenses. If the home inspector finds problems with the home, you have the opportunity to either negate the contract or to renegotiate the sales price.

Have a healthy and properly funded savings account prior to applying for a mortgage. You will need to have cash on hand for closing costs, a down payment and such miscellaneous expenses as inspections, application and credit report fees, title searches and appraisals. Of course, you'll get better mortgage terms if you have a larger down payment.

Pay your mortgage down faster to free up money for the future. Pay https://www.businesswire.com/news/home/20220310005766/en/MeridianLink%C2%AE-Announces-Agreement-to-Acquire-StreetShares%C2%AE when you have some extra savings. When you pay the extra each month, make sure to let the bank know the over-payment is for the principal. You do not want them to put it towards the interest.

Don't take out a mortgage for the maximum amount the bank will lend you. This was a strategy that backfired on thousands of people a few short years ago. They assumed housing values would inevitably rise and that payment would seem small in comparison. Make out a budget, and leave yourself plenty of breathing room for unexpected expenses.

So many individuals all over the world are in search of a home mortgage only to see their application get denied. This does not have to be you, and the tips that you just read have simplified everything. Use them wisely to help you prepare yourself to get approved for a home mortgage.